Wealth management is navigating a period of significant transformation. Shifting investor expectations, rapid advances in AI, growing interest in digital assets, and the increasing mobility of wealth are reshaping how firms serve clients and deliver value. At the same time, regulatory requirements and operational resilience expectations continue to increase, placing greater demands on technology, data, and operational models

As wealth becomes more global, more digital, and more diverse, firms must balance personalization, trust, and efficiency at scale. Those that invest in modern technology foundations, data-driven insights, and intelligent automation will be better positioned to support evolving client needs while maintaining the high levels of service, transparency, and compliance expected in wealth management.

Explore the 5 trends reshaping wealth management

1. Millionaire migration requires global capabilities

Why the movement of global wealth is forcing firms to rethink service delivery, compliance, and client engagement.

2. Private and digital assets drive portfolio diversification

How growing demand for private markets and digital assets is reshaping investment strategies and technology priorities.

3. Digital-first experiences for next-gen wealth clients

The digital experiences younger investors expect and why firms cannot afford to fall behind.

4. Compliance and operational resilience drive innovation agendas

How growing regulatory demands are accelerating investment in smarter, more resilient wealth operations.

5. AI scales advice and raises the bar on fee transparency

How AI is helping advisors scale personalization, improve productivity, and demonstrate value more effectively.

Millionaire migration requires global capabilities

The continued movement of wealth across borders is creating new demands for wealth managers. Millionaire migration has increased from approximately 51,000 individuals in 2013 to a provisional 142,000 in 2025, driven by factors including changing lifestyles, tax regimes, and remote working patterns. As high-net-worth individuals and families become increasingly international, firms must support cross-border advisory services, multi-jurisdictional compliance requirements, and geographically dispersed assets. This is accelerating investment in digital onboarding, remote advisory capabilities, cloud-based platforms, and flexible operating models that enable firms to deliver consistent service experiences while navigating growing regulatory complexity.

Private and digital assets drive portfolio diversification

Portfolio diversification remains a core objective for investors, but the asset classes supporting that diversification are evolving. Demand for private market opportunities continues to increase, while digital assets and tokenized securities are attracting growing interest through capabilities such as fractional ownership, enhanced liquidity, and faster settlement. These developments are creating new opportunities for wealth managers but also introducing greater operational and regulatory complexity. To capitalize on this trend, firms require technologies that support secure custody, compliance, integration across investment ecosystems, and the management of increasingly complex ownership and asset structures while continuing to support active portfolio management in a volatile market environment.

Digital-first experiences for next-generation wealth clients

Generational change is reshaping expectations across wealth management. Millennials and Generation Z already represent nearly 40% of global wealth, while the Great Wealth Transfer is introducing a younger cohort of high-net-worth and ultra-high-net-worth clients with different service expectations and stronger digital preferences. Research suggests that 46% of inheritors switch firms within two years due to gaps in digital experiences. As a result, wealth managers are increasingly adopting hybrid service models that combine human advice with digital onboarding, personalized insights, omnichannel engagement, and self-service capabilities. Delivering seamless digital experiences has become an important factor in attracting, engaging, and retaining the next generation of wealth clients.

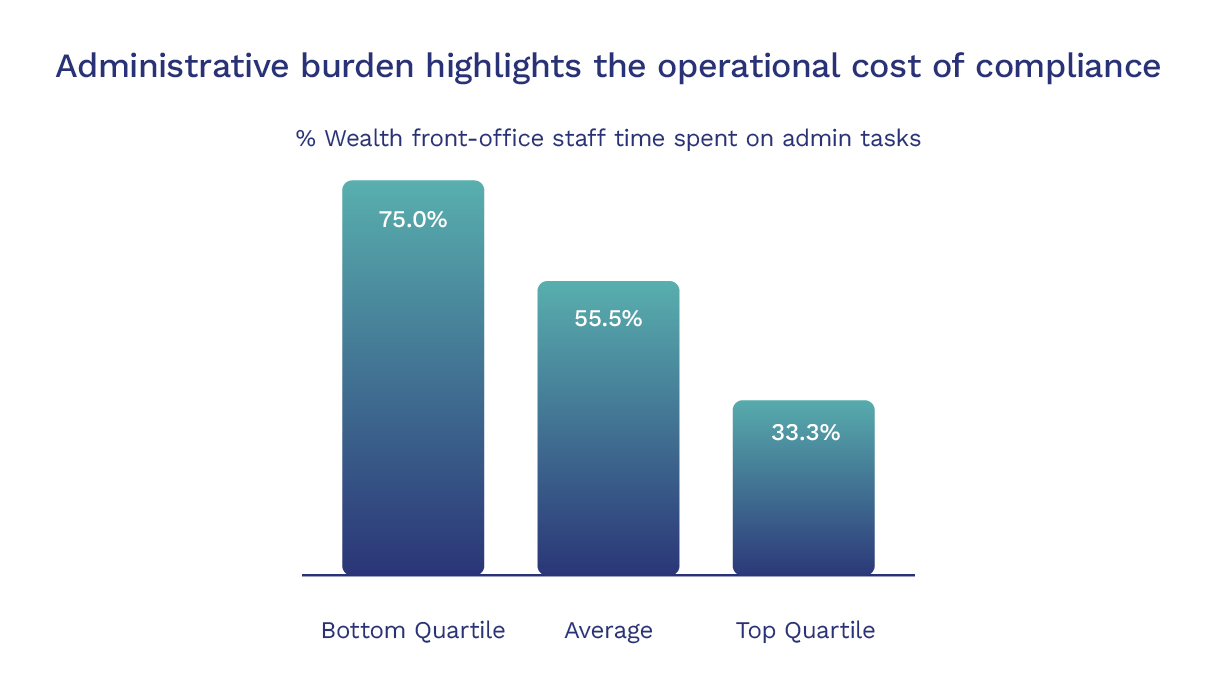

Compliance-driven innovation and operational resilience

Regulatory complexity, operational resilience requirements, and increasing efficiency pressures are driving significant investment across wealth management. Firms must comply with evolving regulations while maintaining transparency, managing risk, and ensuring uninterrupted client service. Temenos Value Benchmark data shows wealth front-office staff spend an average of 55.5% of their time on administrative activities, highlighting the operational burden created by compliance processes. In response, organizations are investing in technologies that support real-time compliance monitoring, perpetual KYC models, AI-assisted due diligence, and greater operational resilience. These capabilities help firms improve efficiency, strengthen auditability, enhance client confidence, and create a more scalable foundation for future growth.

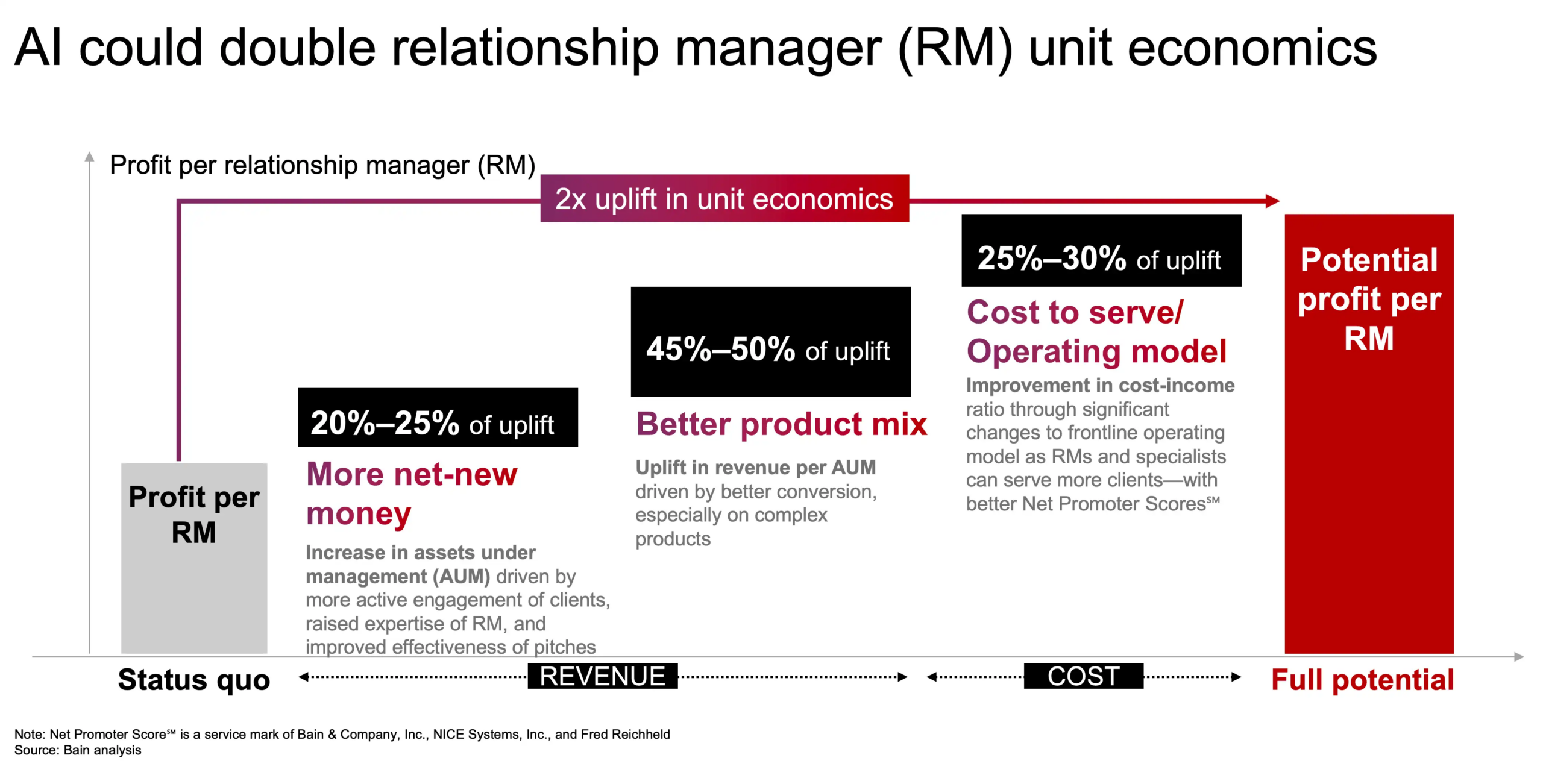

AI scales wealth management advice and raises the bar on fee transparency

AI is reshaping the economics of wealth management. A key mechanism of this transformation is expanding advisory capacity and enabling tailored advice at scale.

For example, AI automates meeting preparation and documentation processes using targeted information, freeing up time for quality interactions with clients and supporting growth in assets under management (AuM). Linking client profiles with product and portfolio insights helps advisors match client needs with products, potentially increasing revenue.

Bain research suggests that AI has the potential to improve unit economics twofold. An estimated 25% to 30% of this uplift will come from reducing non-client-facing tasks, allowing advisors to serve more clients while maintaining personalization and high-quality service at lower cost.

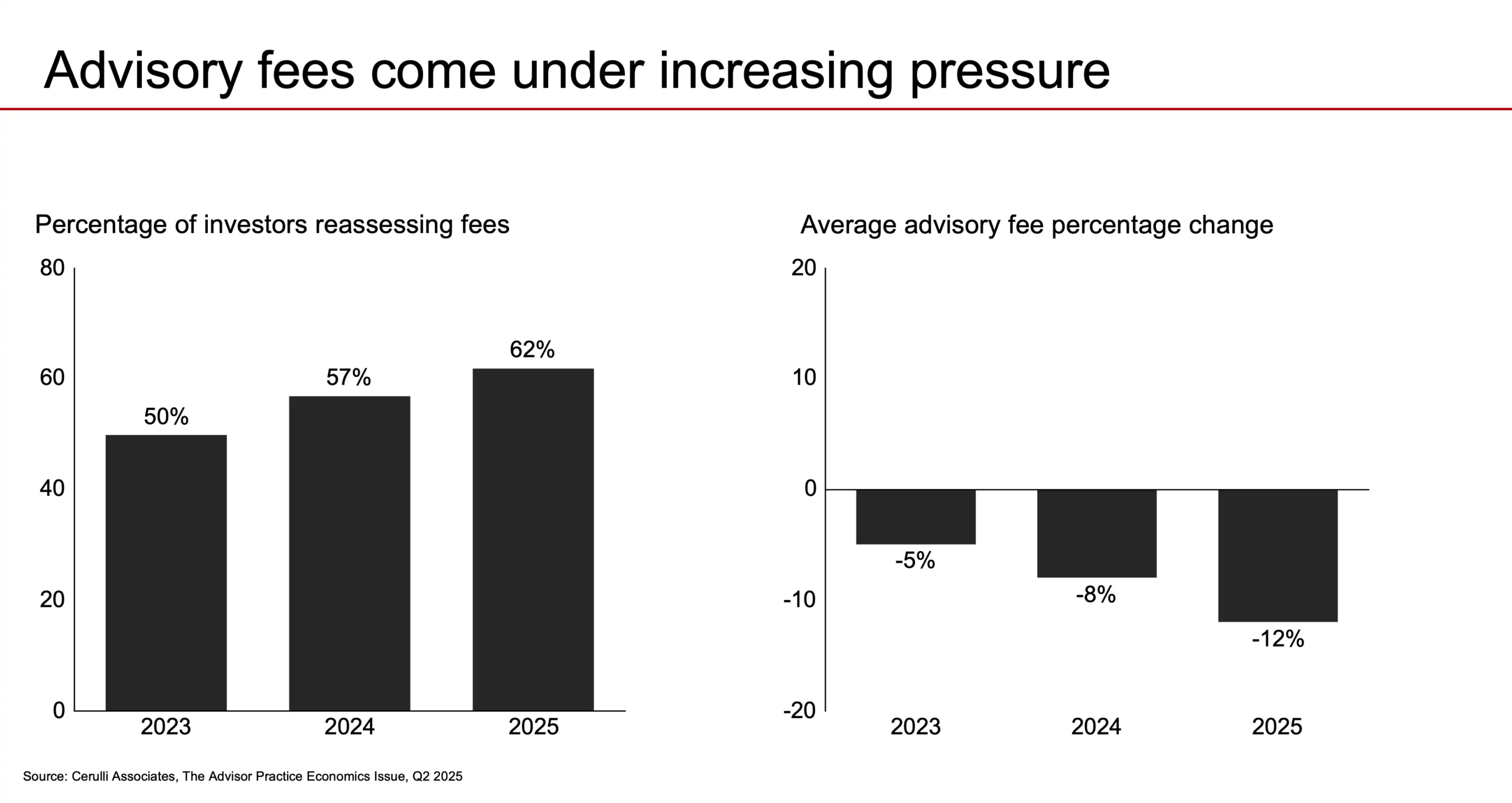

Meanwhile, rising client scrutiny and fee compression are reshaping the economics of wealth management. With 62% of investors reassessing advisory fees in 2025 and average fees down roughly 8% annually in 2023 through 2025, price transparency has become essential. AI is a critical enabler; by automating fee decomposition, benchmarking costs, and real-time client reporting, firms can respond to transparency demands at scale while protecting margins and reinforcing trust. Rather than defending pricing, advisors show value through quantified outcomes.

However, most wealth managers still operate on legacy systems and fragmented data stores not designed for AI requirements. Without foundational investment, AI initiatives remain pilot projects rather than enterprise capabilities.

To win, organizations should:

- modernize their technology foundations around the demands of enterprise-grade AI agents;

- embed AI into advisor workflows; and

- redesign pricing communication to emphasize outcome-based value rather than percentage-based fees.

In the age of AI, the key competitive frontier in wealth management is trust, earned through tailored advice and fee clarity. Firms that combine digital intelligence with human judgment will capture that trust. AI does not commoditize advice; it elevates the value.

By: Bain & Company

References

WSJ – Inside the Invitation-Only Stock Market for the Wealthy

Capgemini, World Wealth Report, 2025