Redefining the Future of Banking: Payments

Payment volumes and real-time transactions continue to explode globally as cash declines and embedded payments proliferate.

The rise in smaller, more frequent payments – such as through bill splitting – are also adding to volumes and squeezing processing capacity. Legacy, batch‑based systems are struggling to provide the continuous availability, real‑time processing, and cost efficiency required for sustainable payments growth.

Meanwhile regulatory clarity is laying the groundwork for the convergence of traditional and tokenized finance. As frameworks mature, confidence is growing to integrate these services into existing payment offerings, including the use of stablecoins and central bank digital currencies (CBDCs) to execute transactions.

At the same time, it has become even harder to keep up with the risk landscape. Banks must balance the demands of speed and scale with protecting customers and the business from fraud and other bad actors.

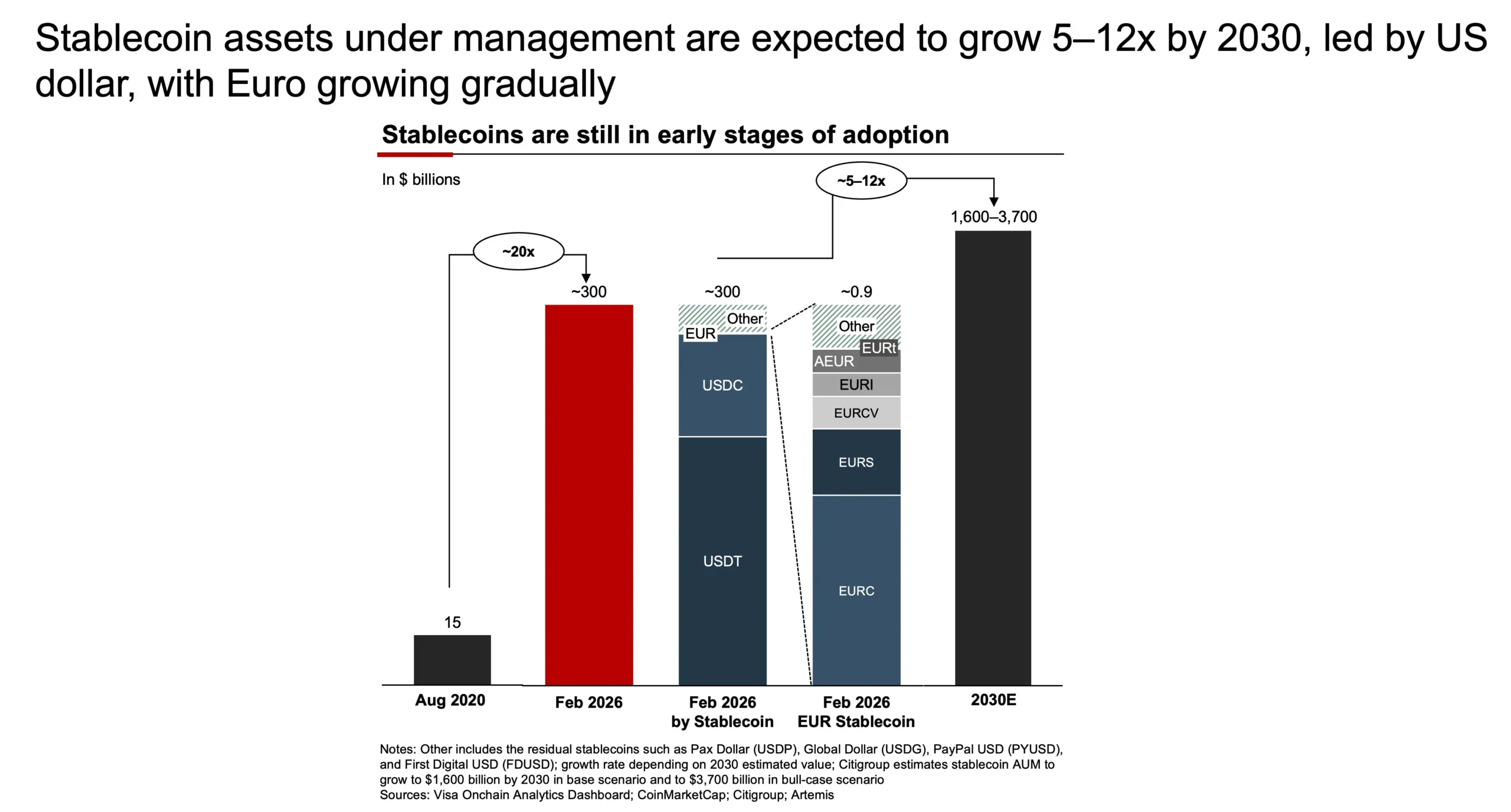

Stablecoins expand into real-world use cases

Stablecoins are moving from crypto infrastructure to a credible settlement and liquidity rail for specific banking and payments flows. In emerging markets with constrained access to stable foreign currency, they are increasingly used to hold value in US dollars. Although stablecoins will not replace existing payment systems, they are becoming strategically relevant in cross-border, automated cash-pooling, and wholesale settlement. For banks, this creates long-term opportunity and near-term complexity.

Scale, regulation, and industry engagement are shaping adoption. Global stablecoin supply has reached $300 billion – still small relative to bank deposits but large enough to prove technical viability and substantial liquidity.

Usage remains largely crypto-native and US dollar-centric, but that’s changing. Clearer regulation in key markets—such as the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act in the US and the Markets in Crypto-Assets (MiCA) regulation in the EU, deeper supervisory engagement, and participation by major banks and payment networks are moving stablecoins from experimentation toward commercialization.

Stablecoins can add the most value where payment systems remain slow, fragmented, or costly. In cross-border and wholesale payments, stablecoins reduce friction in B2B cross-border payments, foreign exchange payment-versus-payment settlement, and collateral mobility. In domestic payment flows where real-time systems or fintechs already offer instant, low-cost, and trusted solutions, stablecoins offer limited value.

Technologically, most banks are constrained by legacy cores, which are not designed for the 24/7 operations and instant settlement that stablecoins provide. In the near term, the shift to stablecoins will require a dual-track model where existing payment rails sit alongside new digital infrastructure, linked by robust integration layers.

Banks should prioritize a small set of high-value use cases and build no-regret capabilities, including custody and wallets, piloting with select clients and partners. The goal is not immediate scale but the readiness for a payment rail likely to grow in importance.

By: Bain & Company

How tokenization and wallets will change banking

Digital wallets are evolving from payment instruments to foundational infrastructure for financial services. As assets and transactions extend beyond traditional core banking systems to digital asset networks, through tokenized deposits, stablecoins, and emerging CBDCs, the conventional bank account is being redefined. Increasingly, it will need to function less as a static ledger entry and more as a programmable wallet capable of securely transacting, authenticating, and managing digital assets and identities.

New products and enhanced services illustrate this trend. Mobile wallets are expanding beyond contactless payments to incorporate digital identity credentials, such as government-issued identities and passports, enabling secure authentication for travel and regulated services.

Meanwhile, crypto wallets support self-custody of tokenized assets across decentralized finance ecosystems, signaling a shift toward customer-controlled financial identity and value storage on digital asset networks.

Institutional products are also emerging. Banks and asset managers are experimenting with tokenized deposits, representations of cash balances on digital asset networks that enable real-time settlement and interoperability across digital ecosystems. Tokenized investment products demonstrate how traditional financial assets are held and transferred via wallets on digital asset networks.

Looking ahead, digital wallets will increasingly incorporate identity management and authentication capabilities based on verifiable credentials, allowing banks to issue and verify identity attributes seamlessly across services. The transition from bank accounts to wallets—blending programmable value, portable identity, and cryptographically assured access—will reshape customer engagement and position banks as a provider of digital trust.

Regulatory clarity accelerates digital currency adoption

Digital currency regulation is taking shape, with the introduction of regulatory frameworks such as the US GENIUS Act and the EU’s MiCA helping to formalize issuance, reserve requirements, and consumer protections.

CBDC initiatives are also gaining ground. Europe’s progress on the digital euro is one of the most significant steps toward mainstream adoption, with 2026 set to be a “crucial year” for the project, and a potential release expected by 2029.[1] Over 100 other countries are also actively engaged in CBDC work.[2]

Against the backdrop of global political turbulence, CBDCs have become increasingly attractive to governments as a way of reclaiming control over payments infrastructure, including rails and data. Their rollout will significantly impact processing and management infrastructures, as currency distributions will need to be tracked and fed to the central bank in real time.

Although it could be years until we see full-scale rollouts, the coexistence of increasingly regulated stablecoins and CBDCs is already helping to define a market structure. Banks and other financial participants such as payment processors are starting to plan for interoperable rails and compliance workflows to support both as digital asset ecosystems continue to mature.

Beneficiary verification adoption accelerates globally

Beneficiary verification, designed to make sure the name provided by a payer matches the recipient’s account name before funds are transferred, have become mandated, standard practice in many markets around the world – and increasingly leveraged within the cross-border space. Financial crime prevention, changing regulatory requirements, and an increased focus on customer trust and operational efficiency are all driving adoption.

Proliferation of beneficiary verification services is putting pressure on payment service providers to support a growing mix of these tools across multiple markets. This is prompting discussions around the standardization and consolidation of services, driven by the need for greater regulatory alignment. More harmonized solutions would help reduce operational burdens – lowering costs and minimizing friction from additional steps – for providers operating across multiple markets.

Real-time efficiency and scalability remain key challenges, particularly as cross-border payment services move to more instant-based delivery. Leveraging cloud technologies for resilience and scalability, while also choosing beneficiary verification service providers that can deliver high performance at scale, will therefore be essential for future success.

AI powers smarter payments processing and compliance

The scale of payments, combined with rising expectations for instant processing and tighter regulatory oversight, is putting significant strain on processing infrastructures, particularly in financial crime mitigation.

With legacy systems pushed to their limit, agentic AI and machine learning are stepping in and increasing speed and accuracy, freeing human teams to focus on high-value decisions (such as assessing an alert for a suspicious transaction). These technologies streamline compliance exceptions by identifying, investigating, and resolving discrepancies, often before they escalate into larger operational or compliance challenges. As mentioned previously, AI agents can also detect and repair broken transactions in real time.

What were once manual, reactive processes are becoming more proactive capabilities. This is also evident in payment initiation, where front-end agentic AI efficiencies are increasing the need for scalability across the whole processing value chain.

As digital challengers adopt these technologies as table stakes, AI has shifted from a nice-to-have to a must-have to stay competitive. However, AI is not a one-off investment; it is increasingly being baked into operating models and is expected to continue evolving not just within payments, but also across financial institutions more broadly.