Explore the 5 trends reshaping retail and business banking

1. Capitalizing on digital banking beyond customer experience

How leading banks are turning digital experiences into growth, loyalty, and share of wallet.

2. A hybrid model for SMEs’ digital future

Why the future of SME banking combines intelligent digital journeys with trusted human advice.

3. Hyper-personalization becomes the new battleground

How AI-powered personalization is transforming customer acquisition, retention, and growth.

4. Driving loyalty with tiered banking experiences

The subscription-style banking experiences redefining customer loyalty and engagement.

5. Connecting traditional banking with decentralized finance

How banks are unlocking new growth opportunities across digital assets, stablecoins, and DeFi.

Retail and business banks are entering a new phase of competition. For years, digital transformation focused on improving customer experience. Today, the conversation is shifting from engagement to economics.

Against a backdrop of changing interest rates, rising customer expectations, and intensifying competition, banks are under growing pressure to demonstrate measurable returns from their digital investments. The opportunity goes beyond acquiring customers or reducing costs. It lies in increasing share of wallet, strengthening loyalty, and creating more valuable, long-term customer relationships. These outcomes increasingly depend on how effectively banks can use data, analytics, and AI to understand customer needs and respond in real time. Hyper-personalization, intelligent recommendations, and more sophisticated loyalty models are becoming critical tools for growth rather than simply enhancements to the customer experience.

At the same time, the operating model of banking is evolving. Customers expect the convenience of digital self-service alongside timely access to expert advice when it matters most. To meet these expectations, banks must continue investing in modern technology foundations that support integrated digital experiences, intelligent automation, and AI-powered decision-making across the customer journey.

The institutions best positioned for the future will be those that successfully combine digital efficiency with human expertise, creating more personalized, scalable, and profitable banking relationships in an increasingly hybrid financial system.

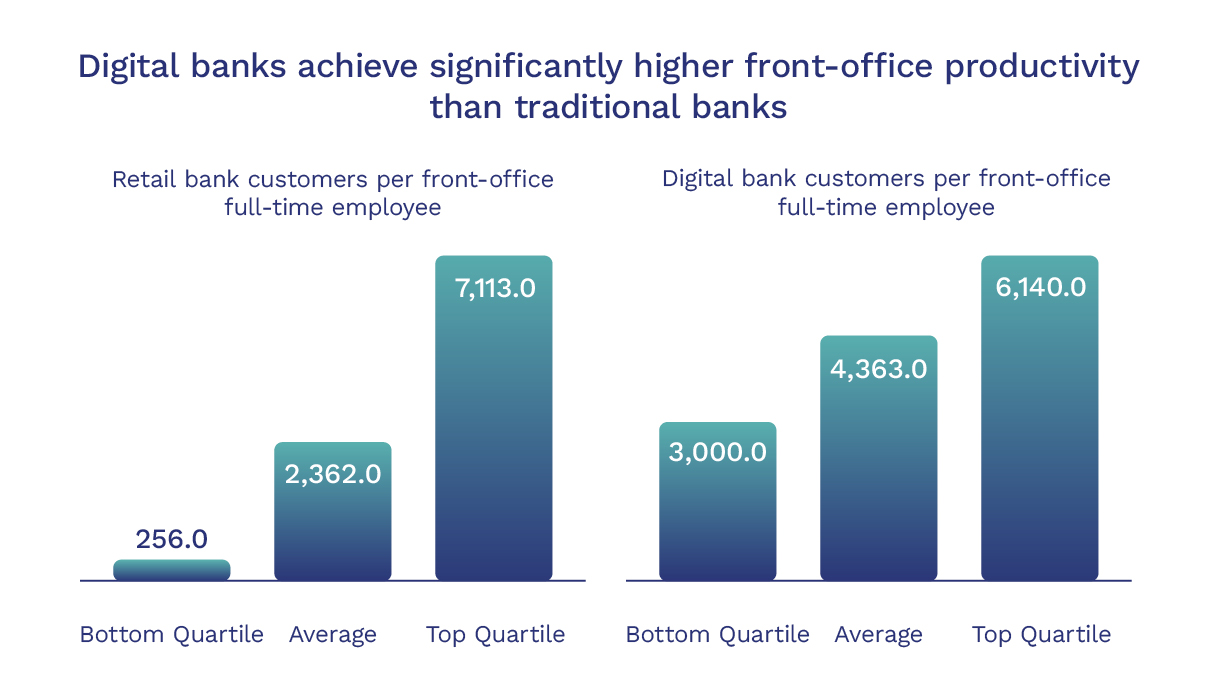

Digital banking enters its value creation era

For more than a decade, banks have invested heavily in digital experiences to improve convenience, trust, and engagement. That investment is now entering a new phase. The focus is no longer on building better digital channels. It is on extracting greater value from them.

Leading banks are using customer data, behavioral insights, and AI-driven recommendations to increase share of wallet, strengthen customer relationships, and identify growth opportunities that would previously have gone unnoticed. The objective is not simply to improve customer satisfaction, but to drive measurable commercial outcomes through more relevant interactions, smarter product recommendations, and stronger retention.

The next chapter of digital banking will be defined by how effectively institutions convert digital engagement into sustainable growth.

A hybrid model for SMEs’ digital future

The future of small and mid-size enterprise (SME) banking isn’t solely digital; it’s hybrid, pairing robust digital capabilities with human advice. Digital offerings and transactions are important, but SME clients continue to value a human touch at pivotal moments. Winning models combine strong digital propositions with relationship managers (RMs) who orchestrate the full experience.

Although most banks already have core digital journeys in place, AI offers the next step-change to make those journeys smarter and more responsive for clients and RMs. Fragmented, manual processes can become end-to-end digital workflows that enable straight-through processing across onboarding, lending, payments, and investments.

But digital alone is not enough. SMEs want the flexibility to self-serve for straightforward tasks while accessing informed, proactive advice from RMs. In the most effective models, RMs are fully integrated into the client’s digital journey. They have visibility into key client actions and use digital tools that enhance productivity and anticipate client needs.

Blending robust digital platforms with AI and RMs isn’t about just adding a chatbot. The advantage comes as AI evolves from pilots into foundational layers embedded across workflows. The combination of speed through digital tools and trusted advice can help banks compete effectively with tech-only platforms.

At the same time, SME ecosystem competition is intensifying. As digital marketplaces and commerce platforms embed banking services into their offerings, lending risks becoming a commodity, which can weaken banks’ relationships and reduce their influence with SME clients. Banks will need to make strategic decisions about where they can provide the right client services and when to double down on advisory moments when depth and trust are crucial.

For banks, digital transformation has become table stakes. But the differentiator is a hybrid operating model that embeds AI into core workflows and focuses RMs on moments of truth.

By: Bain & Company

Personalization is expected. Hyper-personalization is becoming the differentiator.

As digital banking matures, traditional approaches to personalization are losing their competitive advantage. Customers increasingly expect banks to understand their needs, anticipate future requirements, and deliver relevant recommendations in real time.

Advances in AI and predictive analytics are making this possible at scale. Banks can combine behavioral patterns, contextual signals, and customer data to create experiences that evolve alongside the customer. These capabilities are influencing everything from product recommendations and customer retention to acquisition strategies and loyalty programs.

In an environment where products are becoming increasingly commoditized, the ability to make every interaction more relevant could become one of banking’s most powerful growth levers.

Banking moves beyond products toward membership

Competition is increasingly being shaped by the experiences banks deliver, not just the products they provide.

Inspired by the success of subscription-based business models, financial institutions are rethinking how they build loyalty and deepen engagement. Premium banking tiers are evolving beyond rewards and discounts to offer personalized services, exclusive benefits, and experiences tailored to specific customer segments.

This shift reflects a broader change in consumer expectations. Customers now compare their banking experience not only with other banks, but with the best digital experiences available in any industry. As a result, tiered banking propositions are becoming an important tool for strengthening relationships, increasing lifetime value, and creating new recurring revenue opportunities.

Banks prepare for a more connected financial system

The relationship between traditional finance and decentralized finance is shifting from competition to coexistence.

Demand for digital assets, tokenized investments, and blockchain-based payment models continues to grow. Rather than standing apart from these developments, banks are increasingly exploring how to participate safely while maintaining the trust, governance, and regulatory oversight customers expect.

Success will depend on the ability to connect both worlds. Institutions are investing in composable architectures, API-driven ecosystems, secure custody services, and digital asset capabilities that allow them to engage with new financial networks without compromising control.

As digital asset adoption accelerates, banks have an opportunity to position themselves as trusted gateways into a broader and increasingly interconnected financial ecosystem.