Redefining the Future of Banking: Corporate and Commercial

Long characterized by manual, bespoke processes and a slower pace of modernization compared to other banking segments, corporate and commercial banking is slowly catching up. The sector is leveraging technology to operate more efficiently and deliver modern, compelling customer experiences.

The macro-economic environment remains challenging with higher funding costs and ongoing volatility continuing to weigh on corporate balance sheets. These dynamics reinforce the need for technology-driven solutions that equip employees with tools that enhance their productivity as well as those that transform historically paper-heavy processes.

Rapidly changing customer expectations are also catalyzing change. Many businesses are seeking more flexible and alternative financing solutions that reflect real‑time performance rather than historical metrics, while treasurers, for example, expect real-time visibility into cash, liquidity, and risk to strengthen business decision-making and operational resilience.

Lending broadens to include flexible credit

Working capital is under pressure with persistent economic volatility and uncertainty. Many businesses require loans for their strategic ambitions or day-to-day operations, but traditional corporate and commercial lending models often fall short. Lengthy approval processes and reliance on historical data can make it difficult for businesses to access credit.

This is accelerating the adoption of alternative finance structures that respond to changing business circumstances. These include solutions like supply chain finance to optimize cash flow management, leasing arrangements free from large upfront costs, and cash flow or asset-based lending that make credit decisions based on current and future cash flow, as well as considering the value of company assets, such as machinery.

The scale of this shift is evident in the growth of private credit markets, which often finance companies with complex risk profiles, and may accept alternative forms of collateral. Private credit markets were estimated at roughly $3 trillion for 2025 and are projected to hit around $5 trillion by 2029, signaling the growing role of non-bank capital in corporate lending – and its direct competition with banks.[1]

Banks are expanding their offerings beyond traditional credit facilities to provide alternative solutions that better reflect business needs. This also helps them compete against digital challengers that already offer more flexible, bespoke credit solutions.

Unified lending platforms: Building the digital core of corporate lending

Corporate credit remains slowed by fragmented workflows, product systems, and manual hand-offs. A unified lending platform consolidates the end-to-end client life cycle into one digital experience, from origination to monitoring. Combined with embedded AI, it can accelerate decisions, increase transparency, and enable more tailored pricing.

Leading banks will consolidate the entire credit life cycle – origination, assessment, decisions, documentation, and monitoring – into a single digital platform. By standardizing processes across products and geographies, banks can improve turnaround times, reduce rework, and increase transparency across the portfolio.

The second defining feature of unified platforms is embedded AI. Rather than layering AI onto fragmented systems, banks are integrating it directly into the core workflow. AI can pull key data from client financial statements, produce a first-pass credit view, support affordability and sustainability checks, and automatically approve simple, low-risk loans with minimal human intervention. For more complex cases, it flags potential risks and supports credit specialists with structured insights. The shift isn’t from humans to machines but rather from turning a traditionally manual process into human–AI collaboration within a single environment.

Unified lending platforms aren’t just about internal efficiency. They also allow banks to plug directly into clients’ workflows. As lending integrates with enterprise resource planning systems, banks can remain visible either by partnering tightly with those platforms or by expanding their own digital capabilities to deliver a broader, stickier client proposition.

Strategically, banks will need to prioritize budgets and AI enablers to stand up these platforms. IT capital constraints and limited AI talent necessitate the careful selection of areas to embed the capability across the organization. Done well, unified lending platforms turn corporate credit into a scalable advantage, accelerating decision making while preserving the human judgment that clients value.

By: Bain & Company

AI agents transform complex workflows

Corporate and commercial banking has traditionally relied on highly bespoke processes designed to manage large transaction values and elevated risk profiles. As a result, achieving straight‑through processing has been challenging.

Administrative burdens could soon be minimized with the rise of generative and agentic AI, which are starting to orchestrate workflows such as deal structuring, compliance checks, and multi-party documentation. AI agents can interpret unstructured data, coordinate tasks across systems, and deliver real-time insights, improving efficiency and reducing the duplication of tasks in areas historically resistant to or unsuitable for standardization.

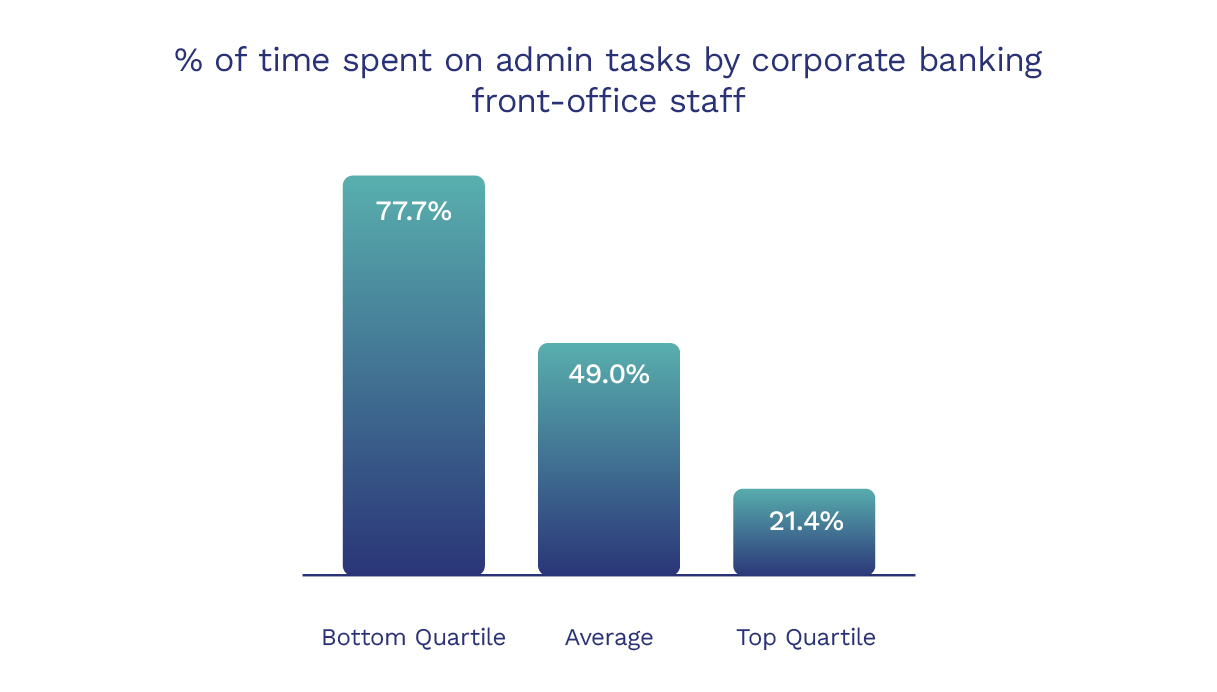

For front-office staff at banks in the bottom quartile, over 75% of their time is spent on admin tasks, which could reduce drastically with the help of modern technology like AI and automation.

However, human oversight and judgement, informed by experience, remains essential in this high-stakes industry.

While widespread adoption will take time, early pilots are expected to reinforce the value of these technologies, laying the foundations for greater efficiency in the corporate and commercial space by 2027. This forms part of a broader industry imperative to modernize technology infrastructure, and transform people and processes.

Treasury redefined by real-time intelligence

Rather than waiting for a daily report, treasurers increasingly expect real-time visibility into cash flow and liquidity to make decisions that help them mitigate risk and maximize growth.

Against a backdrop of economic and geopolitical volatility, as well as fast-moving markets, treasury is evolving from static, batch-based reporting into a live business function powered by real-time insights into payments, liquidity, and cash positions.

As these capabilities become industry standard, banks are increasingly focusing on solutions that give treasurers the tools and insights needed to optimize payments and liquidity. Those that embrace this shift will not only differentiate through increased agility and resilience, but also enhance the user experience by making day‑to‑day tasks significantly easier.

This transformation is unfolding in two main ways. First, financial institutions must elevate the digital experience for treasurers, providing real‑time, API‑driven channels that allow data to be programmatically consumed by specialized ERPs and other treasury tools. Legacy batch‑based mechanisms such as BAI2 and ISO 20022 outputs are no longer sufficient on their own. Meeting today’s expectations requires a robust back‑end infrastructure capable of supporting continuous data exchange.

Looking ahead, technology will continue to play a major role in this central function. A 2024 survey found that 82% of corporates expect AI to support their treasury functions within five years, particularly in forecasting, fraud prevention, and market analysis.[2]

Digitalization moves from advantage to imperative

After years of underinvestment in technology relative to peers, corporate and commercial banking is embracing modernization, and this is expected to accelerate. The case for modernization touches almost every operational aspect – from replacing paper documents and faxes in Europe to phasing out checks in the US, and delivering intuitive digital experiences through treasury management platforms.

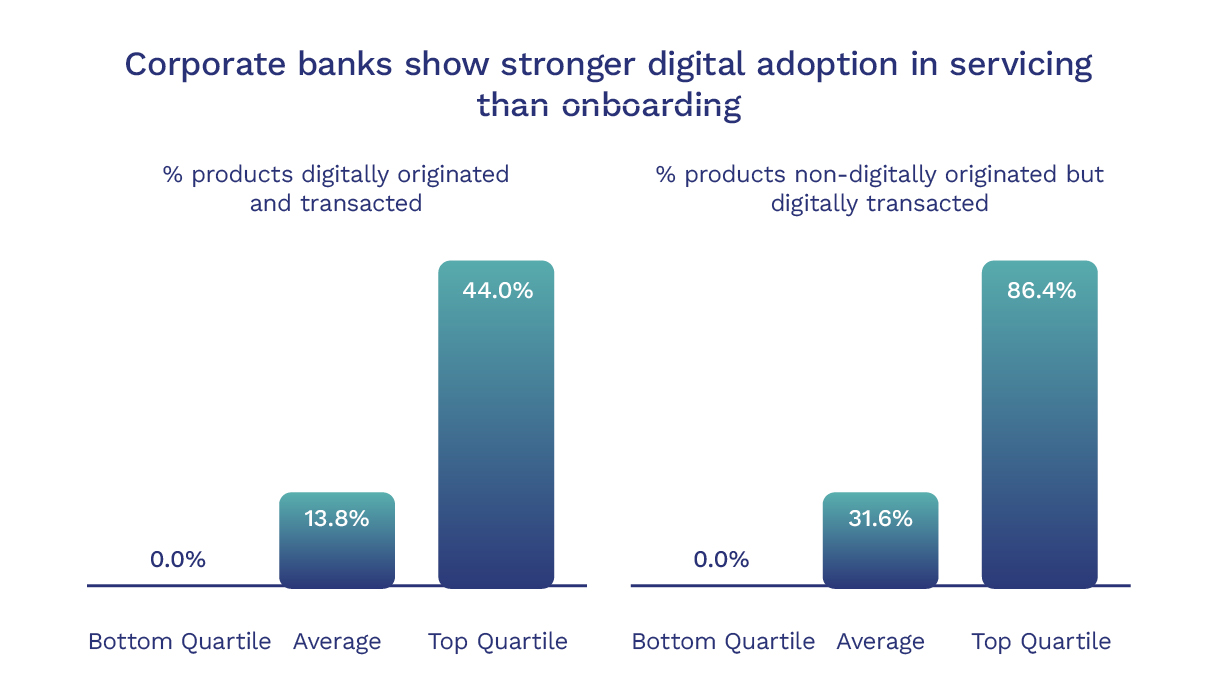

The opportunity to move more decisively into the digital world is clear, with Temenos Value Benchmark data showing that only 13.8% of corporate banking products are originated and transacted digitally, compared to 31.6% digitally transacted but not digitally originated. These findings show significant potential to digitalize processes, with many workflows still reliant on manual data entry, offline documentation, and fragmented approvals. Streamlining these steps through automation, digital origination, and integrated platforms will accelerate decision‑making, reduce errors, and lower operational costs.

Industry analysis suggests that the “consumerization of corporate banking technology is in full swing”, with front-office investments, including digital channels and customer lifecycle management, “front lines” for revamping client experiences.[3]

References

[1] https://www.morganstanley.com/ideas/private-credit-outlook-considerations

[2] https://www.business.hsbc.com/en-gb/insights/innovation-and-transformation/real-time-treasury-smarter-liquidity-stronger-control-and-quicker-decision-making

[3] Celent, Corporate Banking IT Spending Forecasts by Domain 2023–2028