Featured: Featured

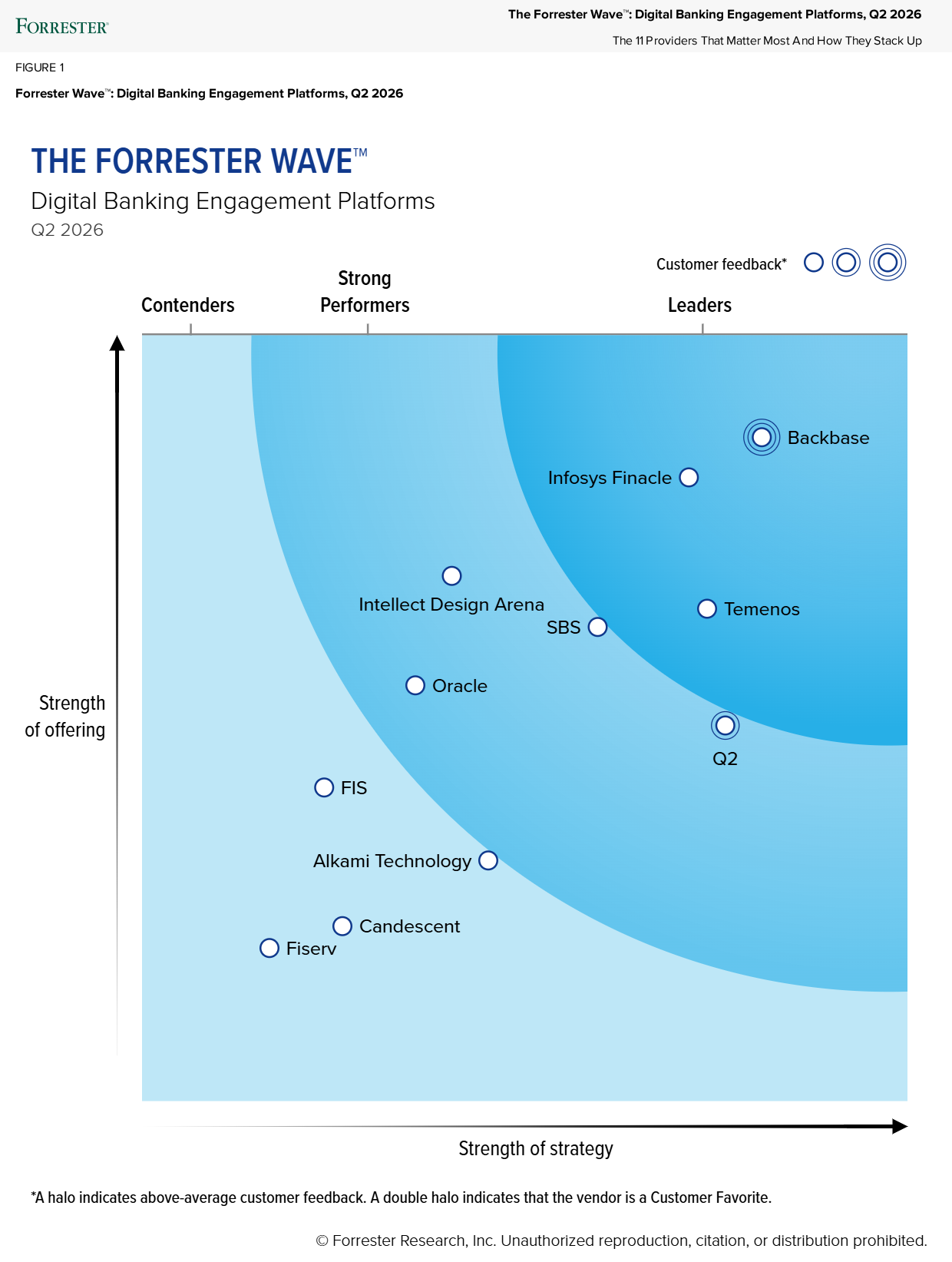

Temenos named a Leader in The Forrester Wave™: Digital Banking Engagement Platforms, Q2 2026

Temenos is positioned as a leader in the Forrester Wave™: Digital Banking Engagement Platforms, Q2 2026. The report scored vendors against 30 criteria relating to both their current offering and strategy.

According to the report

Temenos offers a digital banking engagement platform that is strong on out-of-the-box (OOTB) solutions and multi- and cross-channel support. The vendor supports banks in every region and provides localized ‘microapps’ that are specific to dozens of markets…Temenos is a good fit for banks seeking a wide range of capabilities and a strong architecture foundation.”

Access the report

Forrester does not endorse any company, product, brand, or service included in its research publications and does not advise any person to select the products or services of any company or brand based on the ratings included in such publications. Information is based on the best available resources. Opinions reflect judgment at the time and are subject to change. This report is part of a broader collection of Forrester resources, including interactive models, frameworks, tools, data, and access to analyst guidance. For more information, read about Forrester’s objectivity here.

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

Temenos is positioned as a Leader in The Forrester WaveTM.

According to Forrester, “Temenos invests significantly in an already superior innovation process that includes advanced and explainable AI. {…} Temenos is best suited for banks seeking a comprehensive modern platform with strong AI capabilities, especially those needing guidance on the journey to a cloud and API-first microservices-based architecture.”

Download the report to learn more.

Download the Report

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

Temenos Highwater Benchmark Report

At Temenos, we see our customers building a successful business model around BaaS. Being able to provide financial services, like accounts or loans to brands in Retail and commercial businesses opens a far larger audience. But, with the rapidly rising popularity of embedded finance and BaaS, performance factors come into play: Massive scalability for any transaction volume.

Supporting the needs of future banking models

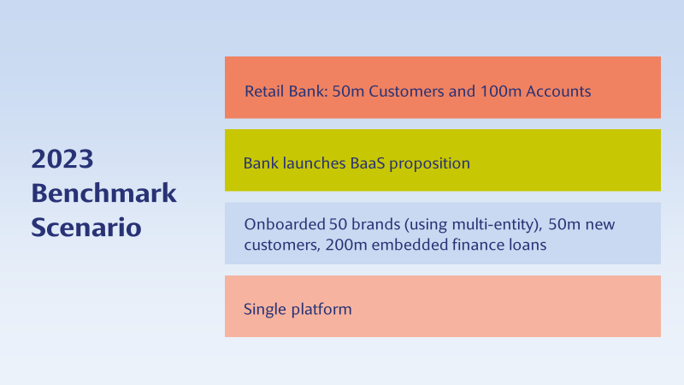

To test the needs of accelerating embedded finance models, we defined the benchmark test scenario for 2023. Th scenario simulates a larger Retail bank that launches a BaaS proposition to open the door to 50 brands. The hypothesis for this benchmark was to support all these banking models on an instance of software on a single platform, processing a representative transaction mix.

Benchmark Partners

Microsoft Azure

In 2011, Temenos and Microsoft were the first in the industry to bring core banking to the Cloud. Today, the partnership supports financial institutions that leverage the Cloud around the world. The combination of the Temenos Banking Cloud and the Azure Cloud Platform enables banks around the world to leverage modern and trusted Cloud technology that can live up to specific requirements in regions, including data regulation, security, and compliance.

MongoDB

Temenos and MongoDB joined forces in 2019 and are on the quest to service the widespread, specific, and strict data requirements that banks need. As Temenos provides its platform for banks around the globe, MongoDB is the trusted partner with a developer data platform that enables financial institutions to innovate faster and build modern applications.

HID

HID provides pre-integration solutions that facilitate integrations and customization with the Temenos Banking Platform. The solutions include identity verification, authentication and real-time risk management for true fraud prevention with a clear focus on offering the best security without compromising on user experience. HID has been a trusted Temenos partner for over 15 years and powers trusted identities of millions of people in more than 100 countries.

View the Highwater benchmark video

Tony Coleman, CTO at Temenos presents the Temenos Highwater Benchmark results.

Explore the benchmarks

Benchmark 2024 press release

The 2024 sustainability benchmark shows the advances in Temenos’ leaner and more sustainable architecture to support banks to meet their sustainability goals.

Benchmark 2023 press release

Temenos processed 200 million embedded finance loans and 100 million retail accounts at a record breaking 150,000 transactions per second on Microsoft Azure with MongoDB database.

Temenos Banking Cloud

The trusted SaaS for 700+ banks around the world. Through the Temenos Banking Cloud, our clients can deliver new services, new features, and changes in an exceptionally short time to market.

Download eBook

Learn more about the Temenos Banking Cloud

Contact us to learn more about the Temenos Banking Cloud and how scalability can help you reach new audiences, efficiencies and drive sustainability.

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

At a Glance

• Just two to four minutes for applicants to complete online credit card origination

• 9% increase in members, from 190K in 2020 to 218K in 2022

• 85% increase in online loan applications in 18 months, from 700 per month to 1,300 per month

• Enables almost-instant issuing of new credit card loans, with auto loans and HELOC soon to follow

• Helps Wescom strengthen its status as a top-ten credit union in California

Wescom Credit Union provides banking with a human touch to more than 220,000 members who live and work in Southern California. Noted for its unique and friendly member experience and ranked among the top 10% of credit unions in Southern California by size, Wescom manages total assets of $6 billion and serves as the preferred banking partner to the students, faculty, staff and alumni of UCLA.

Wescom embraces a model of continuous innovation to help preserve its competitive edge. The credit union identified its online application processes for consumer lending products as one area that it could improve. Starting with credit card origination, Wescom aimed to create an engaging online journey that would match the warmth and friendliness that its members experience during in-branch interactions.

“As a credit union, we are committed to helping our members build better and more prosperous lives. As both interest rates and inflation rise, the quality and extent of what people can afford is impacted. Affordable lending options and reliable banking services can be a lifeline in challenging times. To retain and grow our membership, we’re always looking for new ways to inspire trust.”

Jeff Smrcka, Vice President, Consumer Lending at Wescom Credit Union

Planning a streamlined application journey

Previously, Wescom relied on aging but still functional systems to support its online credit card loan origination process. For members, the process mainly involved filling out time-consuming digital forms. Non-members had to visit a branch in-person to register before applying for their chosen credit card.

Jeff Smrcka says: “Insisting that non-members went through a separate offline sign-up process was a source of friction that few, if any, of our competitors have tackled. We aimed to accelerate the application journey for existing members and allow non-members to join Wescom and apply for credit cards in one quick, easy process.”

Making a positive impact right away

To support the project, Wescom looked for a tried-and-tested solution that would enable a personalized member journey, integrate seamlessly with its main banking infrastructure, and deliver high levels of automation. The credit union decided to use Temenos Loan Origination, an agile loan and account origination platform and decisioning engine purpose-built for creating frictionless application processes.

Wescom used the Temenos solution to plan, develop, and launch the new application journey for its credit card loans. Soon afterwards, the credit union launched a new credit card specifically for UCLA Alumni, with all applications routed through the new streamlined workflow. Applicants fill out the forms via mobile or browser and can use intuitive DocuSign e-signature tools to complete the process. Wescom also made a series of additional configurations to enable front-line staff to complete online applications on behalf of new members who prefer to visit a branch in-person.

“We always aim to embrace leading-edge technologies, and the Temenos solution fit with our vision perfectly. Temenos is at the forefront of innovation, and they are rolling out new functionality all the time. We were especially impressed with Temenos’ API integration capabilities, which would allow our internal teams to pull data from the system easily if needed. They will also help us meet the open banking requirements that will soon reach the U.S.”

Jeff Smrcka, Vice President, Consumer Lending at Wescom Credit Union

Optimizing online experiences

Using Temenos Loan Origination, Wescom now provides a more seamless and convenient origination journey for its credit cards, free from complexity and hassle. Existing members enjoy a faster, more streamlined experience, while non-members can join Wescom and apply for credit card loans in one quick, simple workflow—without having to visit a branch.

The Temenos solution also enables Wescom to achieve much higher levels of automation in its loan decisioning processes. Applicants who enter their details online and meet defined criteria receive automatic approval for their loan, which means their new credit card can be delivered almost instantly to their digital wallet. Moreover, as internal teams at Wescom now spend less time performing follow-up steps with applicants via phone, text or email, they can focus on more productive work.

“Our online application journey for credit card loans now takes just two to four minutes. Previously, the process would take triple that time for members. And for non-members, there is simply no comparison; it is so much faster and easier for them today, and that’s an innovation that few, if any, of our competitors can match. Even in complex cases when an employee has to complete some extra verifications or underwriting, we have increased the efficiency of our workflows by around 20%.”

Jeff Smrcka, Vice President, Consumer Lending at Wescom Credit Union

Fostering innovation

Wescom is now harnessing the Temenos solution to streamline origination processes for other consumer lending products, including personal loans, auto loans, and home equity—as well as giving users more options for secure authentication when completing their application. When the credit union does receive member feedback on their experiences, it can make changes to processes with greater agility and speed.

Jeff Smrcka says: “The Temenos platform is so flexible and powerful that we can quickly bring new services and enhancements to our members. We’re starting to bring every one of our loan products under a single, powerful origination system with Temenos, with auto loans launched later this year and HELOC [home equity line of credit] next year. By drawing on Temenos support, we’re harnessing the full power of Temenos technology.”

Broadening the membership base

Wescom feels confident that the remodeled loan origination process is contributing to strong membership growth. The credit union has seen online loan applications climb by 85% in 18 months, from 700 per month in June 2021 to 1,300 per month in March 2023, comprising applications from both members and non-members. Wescom’s membership has increased by 9% from 190,000 people in 2020 to 218,000 as of December 2022. The UCLA alumni affinity card is helping the credit union gain members across the United States, far beyond its heartland of Southern California.

“The main drivers of our membership growth in 2022 were credit cards and auto loans, which goes to show that the changes we’re making with Temenos are paying off big time. As word spreads among consumers about the ease and speed of our online journey, we expect to see growth continue well into the future. Working with Temenos, we’re enabling more consistent member experiences across every channel: in branch, online and on the phone. Together, we’re innovating to strengthen our position as one of the leading credit unions nationwide.”

Jeff Smrcka, Vice President, Consumer Lending at Wescom Credit Union

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

At a Glance

• Supports 4.5 million customers and secures 33% of the Islamic banking market in Pakistan

• Rises to fourth largest Pakistani bank from 13th in 2009

• 30% faster product development enables innovation and boosts appeal to customers

• 20 times rise in deposits and 400% growth in branch network since 2009

• 90% more online transactions than over-the-counter transactions.

Meezan Bank has achieved a meteoric rise to become the largest Islamic bank in Pakistan. Initially established as an investment bank, Meezan Bank became the first Islamic commercial bank of Pakistan in 2002, with a comprehensive range of Shariah-compliant retail, business, treasury, trade finance, and corporate banking services.

Ali Imran Khan, Deputy Chief Information Officer at Meezan Bank explains: “We aim to be first choice for people seeking financial services without compromising on their faith. By bringing our offerings to more consumers, we hope to improve financial inclusion and create a more equitable society.”

In recent years, the Islamic banking market in Pakistan has become increasingly popular. Although Meezan Bank is the pioneer, there are now many other Islamic and conventional banks with Shariah-compliant offerings. So how has Meezan Bank managed to rise so quickly and maintain its status as the premier Islamic bank in Pakistan? One key factor has been the Bank’s longstanding focus on strengthening its technological infrastructure. Over the years, the Bank has held a longstanding partnership with Temenos.

Aiming for a streamlined and scalable approach

In the years following its launch, Meezan Bank saw consistent growth in customer volumes, deposits, and transactions. Gradually, though, as the Bank’s popularity grew over time so did its demands for an efficient technology strategy. At that time, each branch ran its own servers to record and process transactions. But as the bank expanded to more than 150 locations, there was a need for a more sustainable, less complex and costly solution.

Ali Imran Khan continues: “Our legacy core banking system was decentralized. Customer data was not stored centrally and we had to do extra efforts to enable the online transactions. We continued to add hardware when we opened a branch, which resulted in managing hundreds of servers, taking up valuable time and resources.”

Harnessing a centralized core system

To maintain its upwards growth trajectory, Meezan Bank looked to replace its legacy systems with a powerful, centralized core banking platform. After assessing potential solutions, the bank chose Temenos core banking, engaging Temenos business partner Systems Limited to plan and manage the implementation.

Temenos core banking offered high levels of scalability and the opportunity to implement international best practices. The solution also provided useful multi-book accounting functionality. Temenos works with many leading banks in Pakistan, and Systems Limited has extensive experience working on major transformation projects.”

Ali Imran Khan, Deputy Chief Information Officer at Meezan Bank

During the deployment, Systems Limited helped to familiarize users at Meezan Bank with the tools in Temenos core banking, as Ali Imran Khan confirms: “It’s important to have knowledgeable partners for large-scale projects. Systems Limited and Temenos were excellent: they not only resolved any issues/challenges faced, but also helped us build our internal skillset.”

Enabling seamless fintech integrations

Today, Meezan Bank uses the full suite of modules within Temenos core banking to support its operations—from deposits and treasury services to Islamic trade finance. The bank is also exploring using the open API capabilities of the Temenos platform to integrate with third-party solutions.

The functionality of Temenos trade finance platform is very rich and Temenos is continuously enhancing it, adding integration with other systems, as well as partners. The automation features have significantly reduced processing times, allowing us to handle a higher volume of transactions with unparalleled efficiency.”

Ali Imran Khan, Deputy Chief Information Officer at Meezan Bank

Ali Imran Khan adds: “Islamic fintechs are a growth market in Pakistan, especially in payments and financing. We have already connected our core platform with services from one startup, and we know that it will be quick and easy to onboard others. In time, we expect the Pakistani market to move towards Open Banking; Through continuous investment in digital infrastructure and innovation, we aim to pioneer the future of banking, making it more accessible, convenient, and customer-centric. Temenos core banking gives us the integration capabilities we will need to capitalize on the shift.”

Expanding the scope for innovation

Using Temenos core banking, the bank integrated the core platform with its digital and mobile channels to enable customers to access their accounts, check transactions, and make payments anytime, anywhere.

Innovation is integral to our success, and we invest heavily in research into combining leading-edge banking services with Shariah guidelines, Temenos fits right into this mix. With Temenos core banking, we have reduced time to market for new products by at least 30 percent compared to our legacy systems—which helps us to increase our appeal to consumers.”

Ali Imran Khan, Deputy Chief Information Officer at Meezan Bank

Meezan Bank can now launch a product in 3 to 4 months’ time, previously, it was more than a year.

Reaching millions of customers

Replacing distributed legacy systems with a centralized core platform has made expanding the bank’s branch network much easier. Now, the bank simply onboards new locations to the platform, without adding local infrastructure. Meezan Bank had around 200 branches when Temenos was deployed; it now has more than 1000 across Pakistan.

Enhanced services and a wider branch network have contributed to a much larger customer base: Meezan Bank has more than 4.5 million customers and is now the most profitable Pakistani bank. Meezan Bank also continues to lead the Islamic banking market, with a 33 percent share—When Temenos was deployed, Meezan Bank had just reached the top 15 banks in Pakistan, with deposits of PKR 100 billion; today, it is ranked number four, with deposits of PKR 1.66 trillion. On the digital front, Meezan bank’s transaction volume are growing, with 90% more online transactions than over-the-counter transactions.

Ali Imran Khan continues: “Temenos core banking has been one of the important components in our phenomenal growth. The platform allows us to innovate and seamlessly manage much higher transaction volumes.”

Winning international recognition

Meezan Bank’s success has brought plaudits within Pakistan and beyond. The bank has been named as the ‘Best Bank’ – (2018 & 2020) and ‘Best Consumer Bank’ (2022) at the most prestigious Pakistan Banking Awards by IBP Pakistan, as well as being heralded by prestigious international publications such as Global Finance, Asiamoney and The Banker.

“Temenos is one of our most valuable partners: they are committed to our success, offer an excellent product roadmap and a first-class solution. In our 14 years of operations with Temenos, we were able to roll out numerous initiatives where we had some challenges but with help from Temenos team we were able to resolve these challenges in a timely manner. We look forward to the next stage of the collaboration as we continue to expand our products and services and build a fairer and more prosperous Pakistan.”

Ali Imran Khan, Deputy Chief Information Officer at Meezan Bank

We partnered successfully with

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

At a Glance

• Supports development and launch of “game-changing” services that empower disadvantaged people

• 30-35% growth year-on-year

• 1 million daily transactions and 600K accounts managed seamlessly through Temenos Core Banking for Financial Inclusion

• 63K signups for mobile banking, including 54.3% women and 33.3% from younger demographics

Since 1994, Sinapi Aba has helped financially disadvantaged Ghanaians to build a more prosperous future for themselves. Originally a non-governmental organization providing financial education, Sinapi Aba gained a license to offer savings accounts and deposits in 2013. Today, while Sinapi Aba Trust runs sanitation, apprenticeship, and mentoring programs, Sinapi Aba Savings and Loans focuses on increasing financial inclusion across Ghana.

Aaron Rex Opoku-Ahene, Chief Operating Officer at Sinapi Aba Savings and Loans, explains: “We aim to reach customer groups neglected by larger financial institutions. These include micro, small and medium-sized enterprises [MSMEs], which are often run by women, as well as farmers in isolated rural locations. Our goal is to help them to expand their businesses, build homes, pay their bills, and support their families and local community.”

Hitting roadblocks on the growth journey

Previously, Sinapi Aba managed its lending and savings operations using spreadsheets, stored locally on devices at branches. However, if a device malfunctioned or an authorized user was unavailable to access the right file, business was disrupted and customers requesting a statement went away disappointed. This technology model also made it difficult to scale operations.

King Asante-Frempong, Head of IT/MIS at Sinapi Aba Savings and Loans adds: “For every new customer, we had to create and maintain a new spreadsheet to record transactions and loan repayments. As we expanded, this was becoming unsustainably complex. And relying on legacy systems also restricted our ability to innovate, which was essential for us to bring financial services to more people, especially those that could not easily get to our branches.”

The operating model had drawbacks for internal efficiency and transparency, too. “Preparing close-of-business (COB) and end-of-month reports on our overall lending performance was tough. A member of our team would have to pull together all the spreadsheets from our branches and then calculate consolidated figures, which was very time-consuming, tedious, and error-prone work,” adds King Asante-Frempong.

Adopting a more agile and robust business model

To increase its outreach to underserved communities, Sinapi Aba decided to modernize its technology capabilities. The objective was to replace spreadsheets with a scalable core banking platform supported by a central customer database. After assessing potential solutions, Sinapi Aba selected Temenos Financial Inclusion.

“The modern client-server architecture of the Temenos solution would allow us to transform our operations and adopt more agile ways of working. And the robust processing capabilities were ideal to support high volumes of transactions. Plus, Temenos offered a choice of certified partners with years of experience working with African financial institutions to roll out the platform and train our users.”

King Asante-Frempong, Head of IT/MIS at Sinapi Aba Savings and Loans

Accessing leading-edge core banking capabilities

Since the initial deployment, Sinapi Aba has worked with STRAJ Solutions to complete multiple upgrades of the Temenos platform, enabling access to the latest functionality, integration, and support. Among the most important enhancements that the microfinance institution has gained with recent releases are non-stop 24/7 transaction processing capabilities and a more intuitive browser-based user interface.

“The latest Fixed Assets module in Temenos core banking is really useful, enabling us to automate accounting tasks and remove a lot of headaches for the finance team. Recent upgrades have also streamlined our backup strategy, which helps ensure customer data always remains secure and available.”

King Asante-Frempong, Head of IT/MIS at Sinapi Aba Savings and Loans

Temenos Financial Inclusion also simplifies data analytics and report generation for Sinapi Aba. Rather than spending time scraping data from complex spreadsheets, business users can quickly create reports for senior stakeholders that provide insights into the COB or end-of-month position, the overall performance of the lending portfolio, and other key metrics, such as operational costs.

At any time, Sinapi Aba can call on STRAJ Solutions for additional support. “The training from STRAJ Solutions was excellent, so we have a strong knowledge of Temenos core banking and the Financial Inclusion configuration. Whenever we face challenges, they provide great service and quickly bring in help from Temenos when required,” adds King Asante-Frempong.

Bringing financial services to clients in isolated regions

Sinapi Aba is using the open API capabilities of Temenos core banking to innovate and launch new customer services. For example, the microfinance institution has integrated its core banking platform with the Ghana Interbank Payments and Settlements System managed by the country’s central bank—enabling customers to make instant transfers from their Sinapi Aba account to other banks or digital wallets.

In another major initiative, Sinapi Aba used Temenos to develop a mobile banking platform specifically for underserved customer groups. Available as an iOS or Android app or a USSD service, the mobile offering gives users a secure, accessible, and convenient way to make loan repayments, check savings accounts, pay bills, transfer funds, and more. It also offers access to a series of ‘How-to’ educational videos in multiple languages that help to increase financial literacy and build confidence in managing money.

Although only launched recently, Sinapi Aba has recorded a total of 63,000 customer signups for the mobile banking offering, with 65,000 transactions being made through the app and USSD service every month. In total, 54.3 percent of users are women, and 33.3 percent are from younger demographic groups. Sinapi Aba believes the mobile offering will be a game-changer for financial inclusion.

“Our innovative mobile service helps us reach people in isolated rural areas that cannot visit a branch; instead, we are taking banking to their doorway. We offer access to valuable tools that empower MSMEs to bank their daily takings, or for women to save and build a safety net for their families in case of adversity.”

Aaron Rex Opoku-Ahene, Chief Operating Officer at Sinapi Aba Savings and Loans

Reaching more and more disadvantaged Ghanaians

Today, Sinapi Aba uses Temenos Financial Inclusion to support operations at 44 branches, manage more than 600,000 accounts, and process more than one million daily transactions. “We are achieving an average yearly growth of 30 to 35 percent and consistently hitting our targets,” adds Aaron Rex Opoku-Ahene. “One key factor behind this growth is having a reliable, scalable core system that allows us to manage more and more transactions seamlessly.”

King Asante-Frempong concludes: “We have worked with Temenos and STRAJ Solutions for more than 20 years now, and they remain valuable partners to us and an important part of our success. Temenos Financial Inclusion enables us to develop innovative services that increase financial inclusion and help hundreds of thousands of disadvantaged Ghanaians to achieve a brighter and happier future for themselves.”

We partnered successfully with

STRAJ have walked the digital transformation journey with Temenos clients since 2002, enabling them derive optimum value from their investment in the technology of the day.

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

At a Glance

• Scalable, robust platform upon which to build and integrate innovative solutions

• Exceptional foundation that allows HOPE to continuously adapt and expand digital services

HOPE International is a leading Christian non-profit organization that invests in the dreams of families among the world’s underserved communities. Motivated by the teachings of Jesus Christ, Hope International provides microfinance services, savings programs, and training that help individuals and small- and medium-sized business owners to escape poverty.

Launched in 1997, HOPE International has served more than 2.5 million people worldwide since inception. Headquartered in Pennsylvania, USA, the organization’s microfinance operations and partnerships cover Eastern Europe, South America, Africa, and South Asia, and has disbursed over $100 million USD in loans over its 25-year history.

“Our microfinance institutions help underserved people to build better lives for themselves and their families. We do this through providing loans and savings opportunities to entrepreneurs. We also work alongside of the church to create savings groups in their communities.”

Emmanuel Wuver, Managing Director at HOPE International

Clearing the way to growth

In Africa, HOPE International operates microfinance institutions in three locations: Rwanda, Burundi, and the Republic of the Congo. Recently, the organization has focused more on digital service delivery to reach communities in more remote regions and to create greater efficiencies in operations.

Emmanuel Wuver continues: “We now use our in-house built digital field applications to take customer registration, loan applications, and repayments to people rather than relying on them to come our branches. We are also pursuing an ambitious innovation program, featuring new services and an enhanced client experience.”

Previously, Hope International relied on a suite of legacy applications to develop products and process transactions across multiple microfinance institutions. The organization found tasks such as launching new services, preparing reports and tracking loan repayments complex and time-consuming, and supporting differing platforms was inefficient.

“We had gone as far as we could with our old systems,” adds Emmanuel Wuver. “We decided to look for an alternative that would support our innovation and outreach plans. For example, we were keen to integrate our digital field application and mobile banking channels with third-party solutions—including leading-edge fintech tools—to form a more user-friendly, accessible ecosystem of microfinance services.”

Implementing a platform tailor-made for microfinance

To improve operations at its three African microfinance institutions, HOPE International decided to deploy Temenos Financial Inclusion. Purpose-built to help non-bank financial institutions increase their outreach, the scalable, packaged Temenos solution provides integrated core banking, analytics, and digital channels functionality, and pre-configured workflows to reduce time to value.

Emmanuel Wuver explains: “The Temenos solution offers efficiencies to our work, along with configurable product development frameworks to accelerate innovation. We were also impressed with the open APIs, which make it easier to connect with our commercial partners. The extensive experience of Temenos in the microfinance space was another attraction.”

HOPE International implemented the solution with support from Temenos. The organization started in Rwanda, going live with Temenos Financial Inclusion in just 14 months. Next, HOPE International began the process in Burundi, using a remote deployment process due to pandemic restrictions. After a successful deployment in Burundi, the HOPE team used a hybrid deployment process to implement the solution at their operations in the Republic of the Congo.

“We greatly appreciate the support of the Temenos team throughout the challenges of each implementation. Applying the lessons learned in Rwanda allowed us to go live in Burundi and the Republic of the Congo much faster, despite the impact of the pandemic.”

Emmanuel Wuver, Managing Director at HOPE International

Bringing financial services to people in need

Today, Temenos Financial Inclusion plays a key role in supporting HOPE International’s African microfinance operations. The organization uses the platform for supporting branch services, processing transactions across multiple application channels, managing loan disbursements and payments, and more.

“Our business teams appreciated the flexibility of the Temenos platform, including adding new menus and building product workflows to fit their needs,” adds Emmanuel Wuver. “We have especially appreciated the ability to build internally on the Temenos platform, enabling us to better equip our staff and significantly enhance our operations.”

The organization has launched internal applications for customer registration, loan applications, and loan repayments that have been integrated with the Temenos platform. Additionally, HOPE has been able to connect the Temenos platform with multiple third-party software applications, including mobile banking and government services.

The engagement with Temenos has also helped HOPE International achieve it’s goal to increase its outreach, as Emmanuel Wuver confirms: “Connecting the Temenos platform with our digital field application allows us to bring new services to people in remote communities. The solution really helps us in our mission to alleviate poverty and support people in need.”

Embracing leading-edge fintech solutions

Moving forward, HOPE International intends to harness the API capabilities of Temenos Financial Inclusion to continue to improve its microfinance services. For example, the organization is planning to integrate with innovative fintech tools for credit scoring and identity verification.

“Many of our strategic plans build upon the Temenos platform. We really value the responsive service we receive from Temenos, especially from the Temenos Product Director for Financial Inclusion. We’re grateful for the partnership and support the Temenos team has for our mission to help underserved communities.”

Emmanuel Wuver, Managing Directorat HOPE International

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

At a Glance

• Provides the foundations for the first ever digital-only bank in Singapore

• Enables 83% faster product development than typical core banking platforms

• Requires 50% fewer resources to manage and operate than standard systems

In 2019, the Monetary Authority of Singapore offered its first ever licenses for digital-only banks. Chinese property development company and Fortune Global 500 member Greenland Group and Hong Kong fintech Linklogis saw a golden opportunity to seize first-mover advantage. Together, they developed plans for Green Link Digital Bank, a financial service provider that would set the standard for innovation in Singapore.

Mr. Kuang Mi, CEO of Lianqi Cloud, and the Head of IT, Greenland Digitech (Parent company of Green Link Digital Bank), explains: “We decided to focus on micro-, small-, and medium-sized enterprises (MSMEs) in high-growth sectors such as technology and sustainable construction. Our goal was to provide digital and mobile banking that would enable our clients to access much-needed capital, manage and improve their liquidity and cash flow, and expand their businesses.”

Turning plans into reality

Building an all-new digital bank from scratch was a considerable challenge. The founders wanted Green Link Digital Bank to offer an extensive range of services—from deposit accounts, loans and electronic payments to specialist trade and supply chain financing, and cutting-edge open banking offerings.

Mr. Kuang Mi continues: “We knew we would face strong competition from other agile fintechs that specialize in developing user-friendly, multi-channel banking services. To survive and thrive in this challenging market, we aimed to implement a lean, agile, and cost-efficient operating model that would enable us to focus on digital innovation and foster long-term relationships with our clients.”

Turning plans into reality would require the right mix of robust infrastructure resources and flexible product development capabilities. To move quickly, the team behind Green Link Digital Bank searched for a proven, best-of-breed core banking platform that would help to meet regulatory requirements and serve as a reliable foundation for its online and mobile services. Scalability was another key requirement: once the bank was well established in Singapore, the plan was to expand into other South Asian markets.

Laying robust foundations

After assessing core banking systems from international and local vendors, Green Link Digital Bank selected Temenos core banking running on the Huawei Cloud to support its launch. The bank makes extensive use of the core platform, including Temenos Payments and Temenos Data Hub, for product development, managing client accounts and transactions, and for key back-office and compliance processes.

Greenland Digitech led the implementation of the core platform for Green Link Digital Bank, with support from Temenos and Huawei. The bank went live in just 11 months, as Mr. Kuang Mi confirms: “Temenos delivered exceptional support, ensuring we completed the implementation quickly and efficiently.”

“The Temenos team was very impressive, presenting well and offering helpful guidance when we applied for our banking license. The platform offered all the core functionality we needed to move to market quickly. We also drew confidence from the fact that many leading Asian banks use Temenos solutions, while their international expertise will be especially useful as we scale operations beyond Singapore.”

Mr. Kuang Mi, CEO of Lianqi Cloud, and the Head of IT at Green Link Digital Bank

Breaking new ground in Singapore

Supported by Temenos, Green Link Digital Bank has successfully launched on the market, becoming the first digital-only bank to operate in Singapore. Using product development frameworks in Temenos core banking, the bank has created compelling and relevant payments, lending, and supply chain finance services to help MSMEs to access vital working capital and trade with local and international partners.

At Greenland Digitech, we have considerable experience with other core banking platforms. In most cases, it can take as long as six months to develop, trial, and launch new products. With Temenos core banking solution, we can bring services to market within one month—83 percent faster, which is helping us to make an impact in the Singaporean market and reach clients before competitors.”

Mr. Kuang Mi, CEO of Lianqi Cloud, and the Head of IT at Green Link Digital Bank

The pre-configured workflows in Temenos also simplify systems management for Green Link Digital Bank, as Mr. Kuang Mi comments: “Most core banking systems require customization and additional coding. Temenos core banking eliminates this complex, time-consuming work: we can manage and operate the platform with 50 percent fewer resources than a typical core system, freeing time for more valuable work.”

Forging a nimble, cost-efficient operating model

Running Temenos core banking on the Huawei Cloud is helping Green Link Digital Bank optimize agility and cost-efficiency. “With the cloud model, we avoid the hassle and expenses of managing on-premises infrastructure, and we can quickly deploy additional resources to run testing cycles for new product features,” adds Mr. Kuang Mi. “Using Temenos core banking on the cloud makes us a more nimble operation.”

Furthermore, Temenos Data Hub is enabling Green Link Digital Bank to achieve efficiencies in its back-office workflows, as Mr. Kuang Mi adds: “Temenos Data Hub offers us a lot of flexibility around how we schedule and run our batch processes, and helps us gain a clear view of our end-of-day position.”

Currently, Green Link Digital Bank is using the API capabilities of Temenos core banking to develop and trial open banking services for MSMEs. The bank is running several pilot schemes with clients to test and optimize the new offerings before launching them to the wider market in Singapore.

“Temenos core banking gives us very strong foundations to support our operations. We will continue to build on the platform to create differentiated banking services for MSMEs. With Temenos, we have launched a first-of-a-kind digital-only bank in Singapore, and we have the capabilities in place to innovate, win new business, and scale our operations into other Asian markets when the time is right.”

Mr. Kuang Mi, CEO of Lianqi Cloud, and the Head of IT at Green Link Digital Bank

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

Used by over 300 banks globally (from the global tier 1 to smaller regional Fis), Temenos’ award winning Financial Crime Mitigation (FCM) product family enables banks and FI’s to avoid regulatory fines, detect fraud and mitigate reputational risks whilst improving throughput and optimizing cost all in line with the banks’ Risk Based Approach.

In terms of deployment Temenos FCM allows you to focus on the business problem of financial crime and compliance, offering ultimate flexibility, allowing clients to choose from private or public cloud, On-premise or to be consumed as a fully managed service (SaaS).

Either choose the entire solution or in part to meet immediate needs and pay only for what is used.

Temenos Recognized as a Leader in The Forrester Wave™: Digital Banking Processing Platforms, Q4 2024

Two-thirds of adults have used embedded finance in the last 12 months. Services like Buy Now, Pay Later have seen over $10bn in revenue conceded by banks to big tech and fintech competition. This short demo explores the value and benefits of Temenos for Buy Now Pay Later. PayArrow Bank walks through the challenges of finding a suitable solution and the benefits of a modern solution, including seamless and fast merchant integration, responsible lending with XAI, a pay later solution for existing customers and fast time to market with the Temenos Banking Cloud.