Key Takeaways

- Core challenge = complexity, not digital adoption: Despite strong growth in digital usage and fintech innovation, APAC banks are hindered by fragmented data and inefficient processes, which increase costs, limit AI effectiveness, and constrain growth.

- Modernization focus is shifting to the core: Success now depends on simplifying core systems, unifying data, and embedding real-time intelligence. This entails moving beyond surface-level digital features to scalable, insight-driven operations.

- Retail & SME banking emphasizing outcomes over channels: With digital maturity achieved, differentiation comes from personalized, data-driven experiences that convert engagement into customer value through unified platforms and analytics.

- Technologies augmenting the corporate banking productivity bottleneck: Manual, fragmented workflows reduce frontline effectiveness; banks that deploy AI and end-to-end digital platforms can reclaim capacity, speed up processes, and unlock revenue growth.

- Payments & wealth platforms + AI = competitive edge: Real-time, cloud-native architectures and AI are transforming wealth management and payments. These technologies enable scalability, and better client service. Operational complexity can be harnessed appropriately with technology into strategic advantages.

Introduction

Across Asia Pacific (APAC), banks are moving faster than ever. Customer adoption of digital services continues to accelerate with over 70% of the APAC population now using smartphones for online banking, payment volumes are expected to reach USD 33 trillion by 2031, and around 11,000 fintech platforms are reshaping customer expectations every day. Yet beneath this surface momentum, many institutions are contending with a quieter but more fundamental challenge: complexity at the core.

Two global structural issues are trending and shaping the APAC banking landscape.

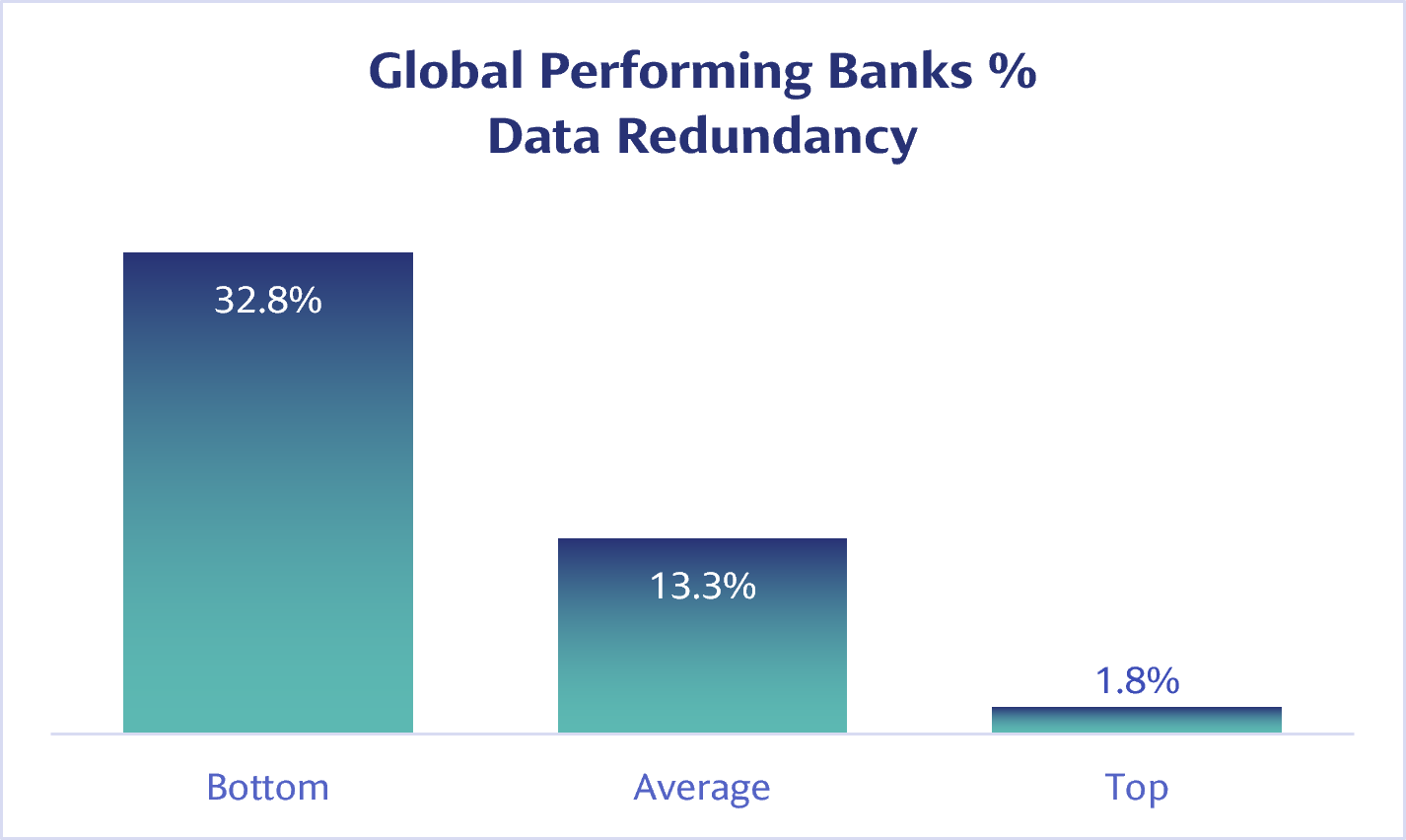

The first is data inefficiency. Despite years of digitization, many global banks still operate with fragmented, duplicated data estates. This redundancy drives up operating costs, undermines analytics accuracy, and limits the impact of AI initiatives.

Temenos Value Benchmark data shows a stark performance gap between top‑quartile banks that have rationalized their data foundations and those still managing duplicated information across systems. In an era where real‑time insight is becoming a competitive necessity, data fragmentation is becoming unsustainable.

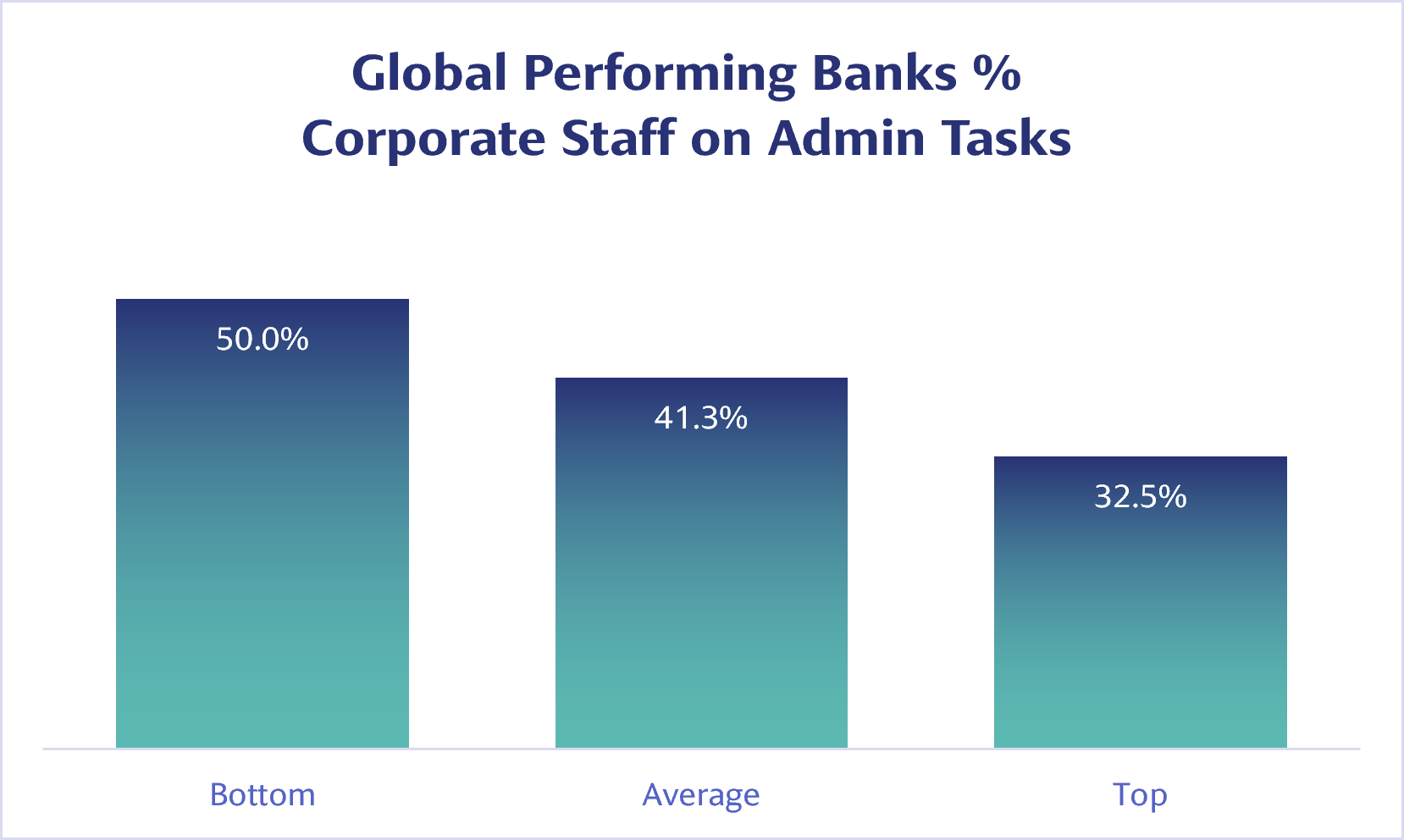

The second issue is human productivity, particularly in corporate and commercial banking. Front‑office teams across APAC continue to spend a disproportionate amount of time on administrative tasks like manual data gathering, reconciliation, and process handovers instead of client engagement and advisory work. At a time of marginal pressure and heightened customer expectations, this inefficiency is directly constraining growth and the revenue potential of corporate and commercial banking divisions across global banks.

Together, these global challenges signal a shift in how APAC banks must think about modernization. The question is no longer what to digitize next, but how to modernize the core so intelligence can scale.

Retail and SME Banking: From Omnichannel to Outcome‑Led Growth

Retail and SME banking in APAC has reached a point of digital maturity. Mobile adoption is high, omnichannel access is expected, and basic digital journeys are expected to be firmly in place. Differentiation now lies in the ability to translate engagement into outcomes.

Customers, particularly Gen Z and digitally native SMEs, expect personalization in real time, consistent experiences across channels, and rapid rollout of new services. Delivering this requires more than front‑end innovation; it depends on a core capable of supporting a unified customer view, flexible product configuration, and embedded analytics.

A leading global financial institution with a presence in more than 40 markets globally has been on a strategic transformation journey with Temenos since 2020 to implement the latest core banking and payments technology across its overseas branches. The bank’s agile architecture provides a robust template for unified branch modernizations globally. By leveraging a single, future-proof composable platform, the financial institution has effectively demonstrated how localized banking capabilities, including retail footprint integrations in strategic hubs like Hong Kong, can be successfully optimized via cloud-native technology to deliver efficient, highly structured customer interactions across the APAC ecosystem.

Conclusively, leading APAC banks are now focusing on embedding insight directly into retail and SME workflows. This includes using data to anticipate needs, deepen relationships, and increase lifetime value. The objective is not to have more digital features, but smarter, more relevant interactions at scale.

Corporate and Commercial Banking: Reclaiming Human Capacity

Corporate and commercial banking faces a different but related challenge. Clients increasingly expect faster credit decisions, real‑time treasury visibility, and seamless digital interaction. Yet internal processes often remain fragmented and manual.

The result is a productivity paradox: highly skilled front‑office staff spend too much time on administration and too little time advising clients. Addressing this requires moving beyond isolated automation projects toward unified platforms that digitize the end‑to‑end credit and servicing lifecycle.

VPBank’s recent core upgrade in Vietnam demonstrates what is possible. Through one of the region’s largest and most complex migrations, the bank migrated more than 18 million customer accounts and millions of loan records under 24 hours. doubled its processing capacity, experiencing a 30% speed improvement in business processing and a 40% increase in payment transaction volumes. and accelerated time to market for new products, all with minimal customer disruption. Core resilience and scalability translated directly into improved front‑office effectiveness.

Across APAC, the strategic priority is clear. Reducing administrative drag through embedded AI and unified workflows is enabling relationship teams to focus on judgment, advice, and growth, creating more value for corporate and commercial banking and freeing up corporate bankers to create more value in contributing to the bottom line.

Wealth Management: Scaling Trust in a Borderless Region

With the intergenerational wealth transfer reaching the shores of Asia Pacific, wealth management in APAC is evolving rapidly as mass affluent and high‑net‑worth segments expand and assets move more fluidly across borders. Clients increasingly expect digital access, transparency, and responsiveness—without sacrificing the trusted, high‑touch advice that defines the industry.

AI is beginning to reshape the economics of wealth management by expanding advisor capacity. Routine tasks such as preparation, documentation, and reporting can be automated, allowing advisors to serve more clients with deeper personalization. But this potential can only be realized with modern core and data platforms that support real‑time portfolio views, cross‑jurisdictional compliance, and seamless digital‑human collaboration. In this context, AI does not commoditize advice. Instead, it amplifies the value of human judgment, provided the underlying foundations are in place.

Other key trends we observe continue to shape wealth dynamics in APAC. Considerations such as a growing preference for digital assets away from traditional assets, a rising need for fee transparency and the ability to demonstrate historic and ongoing value, the ballooning of the mass affluent middle class, and a demand for more complex, non-linear, holistic services requiring wealth management firms to adapt with integrated systems, partnerships, and more client-centric approaches are redefining wealth management practices as Asia experiences its next wave of private wealth transfers and industrial Supercycle backed by global and domestic funding inflows. Wealth managers in Asia Pacific today need to tap on technology to effectively scale trust, to capture this momentous opportunity.

Asia represents a key market for Julius Baer, one of the oldest and most prestigious Swiss private banks. To drive growth in the region, where it provides investment management and advisory services to high-net-worth clients, the bank’s division in Asia deployed Temenos Wealth. The solution combines core banking, portfolio management, digital channels, and analytics functionality in a single platform. With the Temenos solution, Julius Baer is well-placed to deliver high-quality customer service and increase operational efficiency. The project also represents another important step in its partnership with Temenos, following the implementation of Temenos core banking for its business in Luxembourg.

Payments: From Infrastructure Strain to Strategic Platform

Payment volumes across APAC continue to grow at pace, driven by real‑time payments, digital wallets, and cross‑border commerce. At the same time, fraud risks and regulatory scrutiny are increasing.

Legacy, batch‑based systems struggle to provide the always‑on availability, scalability, and intelligent exception handling required for these new payments environment. As stable coins, tokenization, and programmable money move closer to mainstream adoption, payments are increasingly becoming a strategic platform capability, not just a processing function.

Varo Bank is re-imagining personal banking. Launched in 2018, Varo is the first consumer fintech granted a national bank charter in the US. Its mission is to improve the financial lives of its customers with a unique range of high-yield savings accounts, spend tracking and cashflow. Varo provides innovative digital banking services to 180 million Americans currently underserved by the traditional system. For its efforts, Varo Bank have been honoured in 2023, 2024, and 2025 on the Inc. 5,000 placement with a notable 101% three-year growth rate. Partnering with Temenos has also directly improved Varo’s cost-to-income ratio, its deployment of the Temenos Payment and Banking Cloud solution have resulted in an up to 30% cost reduction. It’s successful implementation of the direct payment infrastructure has earned it the Celent Model Bank of the Year. Varo demonstrates that Banks investing in cloud‑native, event‑driven architectures will be better positioned to turn payments complexities into competitive advantage, with contributions to the topline.

The Road Ahead for APAC Banks

Across segments, the pattern is consistent. Banks that simplify their cores, reduce data duplication, and embed intelligence into their operating models are pulling ahead. Those that continue to layer innovation onto complex legacy environments face rising costs, slower execution, and constrained returns from AI.

In APAC, modernization is no longer an IT agenda. It is a business imperative centered on freeing data, people, and intelligence to scale. Today, technology remains central to a bank’s ability to build trust, compete, and grow. Those treating technology as a strategic asset are well poised to pull ahead, and their comparative peers are finding it increasingly difficult to keep pace.

Read the full global report, Technology Trends Redefining the Future of Banking, to explore the insights shaping the next era of banking.